Often the ideas in a blog post spring out of a conversation with a client or colleague, and this one is no different. So James, this one is for you.

Debt is expensive, and your lender needs to make a return on their money so they aren’t going to give you interest on cash you deposit with them of more than they’re taking off you in loan interest or they’ll soon be broke.

So why borrow at all?

Reason one is to enable you to buy something now and pay later. Your house is the obvious example.

The second reason is to invest. If you can make a return on the borrowed cash of more than the cost of the loan, you’re in profit.

The problem is that generating a return of more than your loan interest rate can only usually be done by accepting more risk. The scale of this risk will determine your willingness to borrow.

If the money is going in to your own business you might think the risk is worth taking. If you can borrow £x and turn it into £10x or £100x that sounds like good business.

You could put the money into shares or similar investments. The returns should be better, but there’s no guarantee, and the value of your borrowed investment can fluctuate wildly.

If you’re using mainstream investments borrowing to invest might still be an attractive strategy. The return on a well-managed mixed portfolio (shares, bonds, etc) has averaged several percent a year more than the average mortgage rate for decades, so profits should be forthcoming.

By far the most popular form of borrowing to invest is to purchase investment property. Whilst the returns aren’t spectacular, the income you’ll receive from renting out your house or building is reasonably predictable. You’ll be able to work out the return for yourself.

Investing in property has some other important features. Firstly, it’s easier to get someone to lend you the money in the first place. Lenders are happy to take property as security for your loan, and if you can’t keep up the repayments they could grab it back and sell it to get their money back.

Secondly, interest payments on property investments can usually be set against the rent for tax, reducing the true cost of borrowing significantly, especially if you pay tax at the higher rate.

The third reason is one of psychology. People view property investments as long term so they tend to worry less about swings in the price of houses or buildings. They will ride through economic downturns and tough times to get the benefit of long term growth.

There are very few lenders, on the other hand, who would accept your share and bond portfolio as security, so you’re restricted to either borrowing lesser amounts in the form of a personal loan, or using a property that you own as the security the bank will require. I’m not sure there’s a lot of sense in this rule, but that’s how it is.

Your share portfolio will probably require tougher nerves, too. The sheer visibility of share prices is a big reason why many people don’t stay the course. They are much more likely to cash in when times are bad instead of riding through the ups and downs to get the returns that come through over time.

So is it worth it? Let’s put some numbers on the table to show what’s possible.

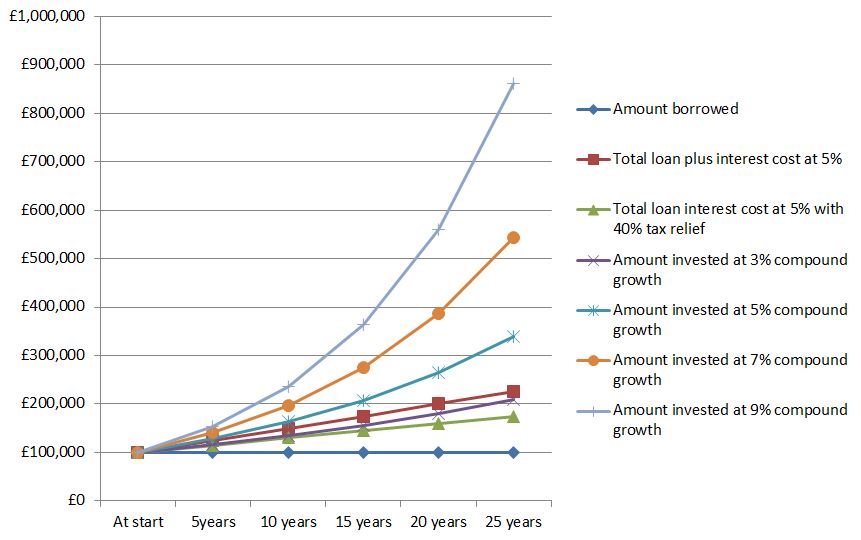

Let’s say you borrow £100,000, in the form of a mortgage on your existing property, at a loan interest rate of 5% a year. Here are the figures:

|

At start |

5years |

10 years |

15 years |

20 years |

25 years |

| Amount borrowed |

£100,000 |

£100,000 |

£100,000 |

£100,000 |

£100,000 |

£100,000 |

| Total loan plus interest cost at 5% |

£100,000 |

£125,000 |

£150,000 |

£175,000 |

£200,000 |

£225,000 |

| Total loan interest cost at 5% with 40% tax relief |

£100,000 |

£115,000 |

£130,000 |

£145,000 |

£160,000 |

£175,000 |

| Amount invested at 3% compound growth |

£100,000 |

£115,927 |

£134,392 |

£155,797 |

£180,611 |

£209,378 |

| Amount invested at 5% compound growth |

£100,000 |

£127,628 |

£162,889 |

£207,893 |

£265,330 |

£338,635 |

| Amount invested at 7% compound growth |

£100,000 |

£140,255 |

£196,715 |

£275,903 |

£386,968 |

£542,743 |

| Amount invested at 9% compound growth |

£100,000 |

£153,862 |

£236,736 |

£364,248 |

£560,441 |

£862,308 |

Or, to show it another way:

Interestingly, even where the loan interest and the return achieved are similar (as shown by the 5% less tax relief and 3% growth lines) the investment return still outstrips the loan interest cost over time. This is because of the compounding effect of the investment, whereby interest is earned on interest.

What this says is that if you could get a return of, say 7% a year whilst paying interest of 5%, over 25 years you would have made a profit of £317,743 in total, and if you could get a 9% return you’d be ahead by £637,308.

Of course it also shows that if your return is only 3% a year you’d be £15,622 worse off in total, although you would still have £109,378 left over if you paid off the outstanding loan at that point, because you’ve paid the loan interest along the way.

So should you follow this plan to get rich? As always, the answer is – it depends. There are a few questions you’ll need to ask yourself before you start. Here are some of them;

- Are you able to borrow the money in the first place? If the amount you want to raise is substantial you’ll probably need something to offer as security and you’ll need to show how you propose to make the repayments.

- Can you afford the repayments? Do you know how much they will be and how to calculate them?

- What will happen to your plan if the loan interest rate changes? Could you afford the extra commitment if the loan cost doubled, say? There was a period in the 1990’s when interest rates reached 15%. If that happened again, how would you cope? (everyone taking out a mortgage should consider this question, by the way).

- Do you know what the likely return on your investment will be?

- Do you understand how secure your invested capital will be? What’s the risk of losing some or all of it? Do you really understand what you’re getting into?

- Are you prepared for the inevitable swings in market prices and investment values? For example, an investment in shares would have returned around 9% a year over the last 20 years or so, but there were some years when values were down to almost half their previous level. Do you have the stomach for that kind of ride?

- Will you need to borrow for any other reason? If you’ve used up all of your credit line you’re going to have to sell something or do some tough negotiating to free up cash in the future.

- Are there restrictions or time penalties involved in either loan or investment terms? If your lender decides they want you to repay the loan immediately and you’ve put the cash into something that won’t pay out for five years you have what we call ‘a problem’.

- Is it worth it? Does the extra money you’ll make justify going through all of this work?

- Do you have the necessary skills to get the required returns for yourself? Or if you are giving the money to someone else to invest for you, have you carried out thorough (and I mean thorough) due diligence on them? Even the most plausible of people and finest of institutions can go pop or get their sums badly wrong, witness Lehman Brothers, RBS, Equitable Life, Tesco, etc., etc., etc.,…….). If in doubt pay for really good professional advice.

- If you’re dealing with an adviser; Do you understand the difference between sound advice and a sales story? Be especially careful of advisers who try to educate you. Here’s a quote from the Dalbar Report (dalbar.com); “Investor education….. has been used as the vehicle to transfer responsibility from the expert to the unwitting neophyte. By providing education, the investor is expected to make prudent decisions that relieve the expert of any responsibility. This use of education as a litigation defence may be effective in arbitration, in the courts and with regulators but it does nothing to protect the investor from making bad decisions.” I couldn’t have said it better myself.

- What does your partner or spouse make of your plan? Trust only goes so far. Full communication is better.

- What is there about your plan that is so obvious that you’ve overlooked it?

Having tried to scare you with what could go wrong, don’t forget that you don’t get to win the trophy by sitting in the changing room twiddling your thumbs. If you’ve answered these questions carefully you should be prepared and be able to avoid the worst mistakes. Having decided, stick with your plan! Persistence is one of the keys to successful investing.

Good luck!